Issue 19

Highly Rated

Standard & Poor's originated in 1860 with the publication of financial statistics on the railway companies in the United States. We began rating the debt of corporate and government issuers more than 75 years ago. Today, Standard & Poo r's Ratings Services has over 750 analysts working from 16 offices in 12 countries. We rate approximately $10 trillion in outstanding bonds and other financial instruments issued by obligors in 50 countries.

What Does a Rating Really Represent?

At Standard & Poor's, om ratings are meant to be an indication of the LkeW10od that a company will repay its debt on time. Our ratings also give some weight to the issue of ultimate recovery, but the key criterion is timeliness.

The overall credit risk is a combination of the business risk and the financial risk of the firm we are rating. The business risk, which accounts for two-thirds of our evaluation, is a composite of the risk prevalent in, say, the mining industry, and of the firm's position with.in that industry. More about that later.

Once assigned a rating, a company is in effect placed on a global scale that facilitates comparisons across industries and cow1tries. The rating has become an essential tool not only for raising capital but also a key component of cross-industry benchmarking.

Standard & Poor's rating scale goes from AAA - corresponding to "rock-solid credits", no risk at all - clown to D, which means default. We add "+" and "-" to each category so that the scale has 20 notches in all. The last investment-grade category is BBB. The risks of default (a late or non-payment of interest or principal) go up very quickly as one enters the speculative-grade range, from BB to CCC. For example, an investor buying into a portfolio of bonds all rated double by Standard & Poor's should expect, based on historical evidence, to be paid back on time in 80% of cases after 15 years.

In other words, we still expect companies to perform well in a great majority of cases, even in some of the speculative grades.

It is also worth noting what Standard & Poor's ratings do not represent. The most usual warning we give is that our ratings are not a recommendation to buy or sell securities. Likewise, we are not advising a company's management on what strategy they should follow. Ratings are not a guarantee against fraud, are not an audit and are not driven only by financial ratios.

Who Needs a Rating?

Any company that is seeking to raise capital in the forn1 of a capital market bond issue, a syndicated bank loan or an international private placement can make use of a rating. Historically, it is the dominance of the US capital market that made ratings often essential to successfully raise capital. However, in Europe and the rest of the world, ratings are also becoming one of the most efficient ways of raising a group's international profile and managing counter-party relationships. For example, in mining and other project-based financing environment, ratings are often needed to demonstrate a firm's creditworthiness at the bidding stage.

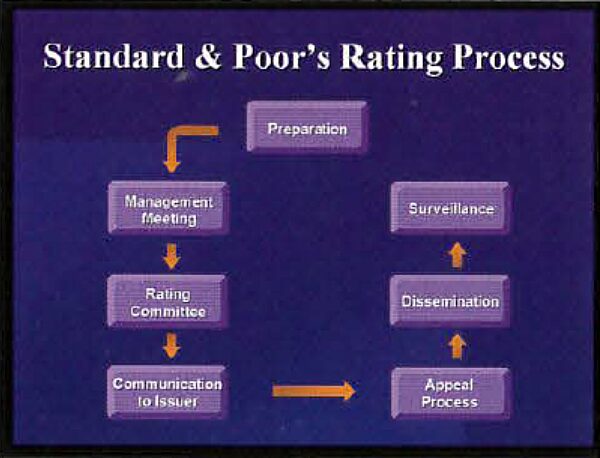

The Rating Process

First, a team of the analyst will visit the company and prepare a rating presentation to the committee that will vote and assign the rating. The issuer is in control throughout the process and can decide to keep the rating confidential, except if making a public issue in the US. Once the rating is public, however, it can go up as well as down, and we will insist on on-going surveillance, including yearly face-to-face meetings, to maintain the rating's accuracy.

The committee will consider both the business risk and the financial profile of the company. The key driver will always be a business risk. Once a business-risk score is agreed upon, the financial characteristics are looked at. In short, this second part of the exercise mainly consists of answering two questions: "Just how much debt is the company going to take on? And how much cash flow doe it generates to service the debt?" In this context, a long track record of tight financial management and adherence to an announced financial policy goes a long way towards convincing Standard & Poor' that a higher rating may be justified.

The Mining Industry

Standard & Poor's considers the mining industry and mining companies as presenting a high degree of risk relative to other areas (such as utilities). The mining industry is characterised by the risks inherent in constructing and starting a new mine, uncertainty regarding the consistency of an ore body and technical operations. In addition to these concerns, the cyclical nature and heavy ongoing capital expenditure requirements of this industry also contribute to increasing its risk profile. Moreover, when a single-mine -site project, as opposed to a mining company, raises debt, it introduces incremental risks such as a lack of geographic and mineral diversity and limited financial flexibility.

However, high ratings can be achieved thanks to potential mitigating factors, such as having a conservative financial structure, a large and mature asset base, reserves with low producing costs, good diversity and a strong track record - for us, these are the keys to success.

Financial Risk

When assessing a mining company, we analyse the company's financial profile. Of primary importance to any rating are the financial projections and the related sensitivity analyses. Standard & Poor 's focuses on the financial leverage levels, the sufficiency of cash flow to service debt payments, and on the entity's financial capacity to sustain adverse operational and commodity-pricing scenarios. We will assess the mine's ability to alter its cost structure in relation to potential commodity price changes and the effectiveness of any price hedge or guaranty incorporated into the transaction.

We will evaluate each company or project in its context. It is unlikely that any company or project would be able to have a higher rating than that of the country in which the majority of its assets are located.

Macro considerations

- Standard and Poor's view on gold is influenced by these key macro economic drivers:

- Outlook for the supply and demand balance

- Secular trends towards lower consumption of the metal

- Central banks' and other larger holders' attitudes towards their reserves

- Production costs across the industry compared to the current price of gold.

These factors will be far more influential than financial ratios alone, though we consider ratios nonetheless.

"Gold Company" Ratings

Standard & Poor's rates 17 companies involved in gold or silver extraction, shown in the opposite table.

Here follows a breakdown of two of the ratings: First, Barrick Gold, with a long-term rating of A and the stable outlook is clearly a very safe credit. The ratings recognise Barr ick Gold Corp.'s position as one of North America's largest and lowest-cost gold producers. Barrick has one of the largest gold reserve bases and has four operating gold mines in Canada and the United States and the fifth mine in Peru - which provides significant geographic diversification. ln addition, Barrick's financial profile is strong, reflecting a conservative financial policy and a well-established gold-hedging program, which helps minimise fluctuations in the gold price.

At the other end of the scale, Coeur d'Alene is rated single Band carries a negative outlook. The ratings reflect a weak business position as silver and gold producer and a very aggressive financial profile. CDA is a relatively small precious metals producer. It has a significant production concentration risk and the company's costs remain well above industry norm s. The company's debt leverage is also very aggressive.

Conclusion

Standard & Poor's is a leader in credit rating world-wide. Teams of analysts follow the same industrial sector in Asia, Europe, and North and South America. What this means is that we speak with the CEOs and CFOs of the top companies in nearly any given industry across the globe. This gives us access to confidential information that we keep to ourselves but use to make comparisons. We derive mu- ratings from these conclusions. We don't claim to be more knowledgeable in an industry than our clients are - but because we speak to so many, we do have a privileged position in assessing each company. Our independence and objectivity are what makes us a useful intermediary in the financial market.