Issue 41

$1,000 for 31 Grams of Platinum: No Panic, but Raised Eyebrows

It is no secret that platinum group metals are scarce goods these days. Only 205 tonnes of newly mined platinum, 235 tons of palladium and 23 tons of rhodium reach the international markets each year. Their limitations in supply contrast sharply with their growing popularity in industrial uses. The precious white metals play a vital role in most modern industries – automotive, glass and chemical – either because they form part of the end product or are bound into the production process. Their attraction is not jewellery buyers and investors as well.

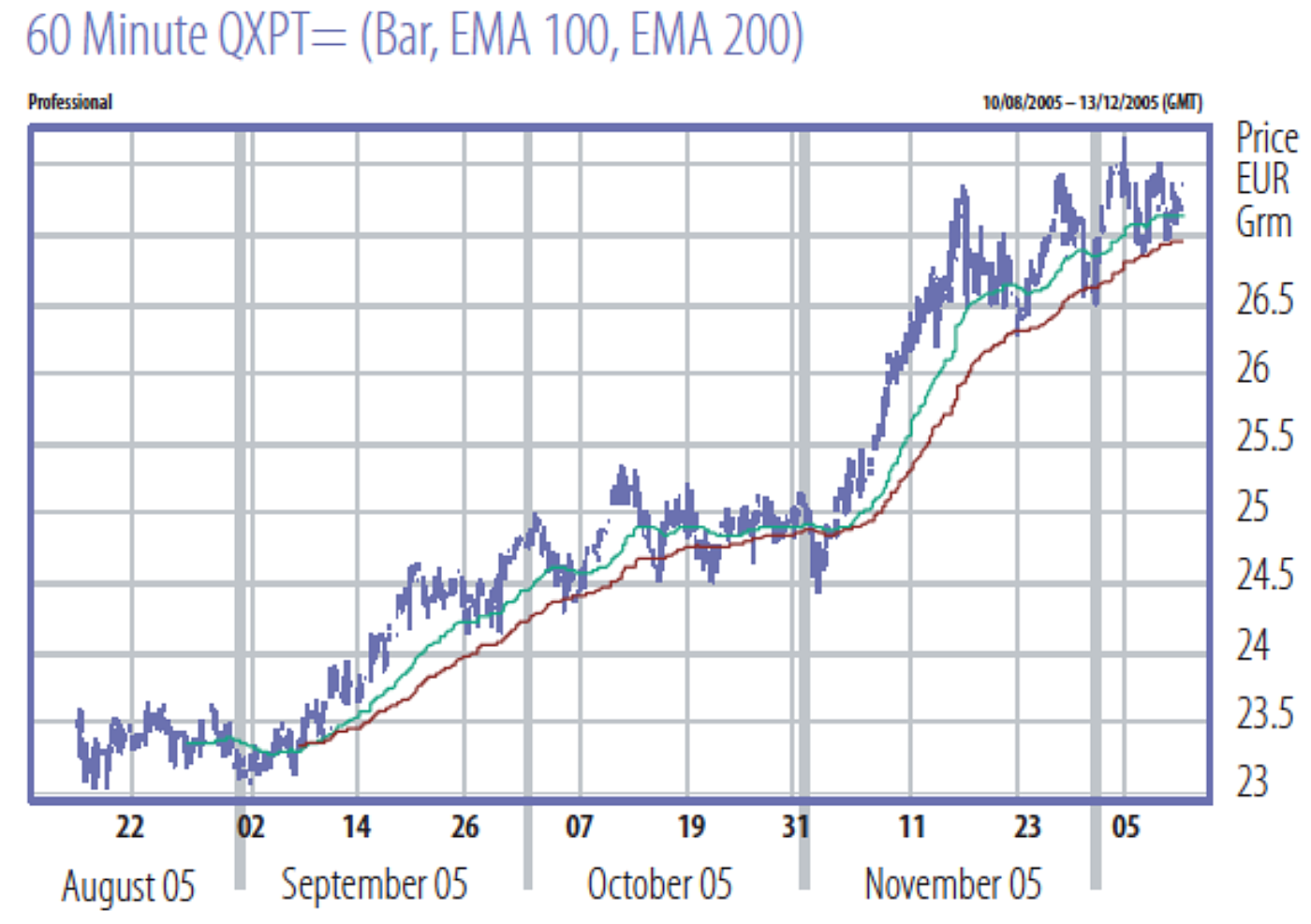

It is therefore no surprise that the combination of global economic growth, increasing investor interest and restrictions on supply led to a massive surge in price for pgms and other metals in recent months. Platinum is a leading example, reaching 25-year highs above $1,000 an ounce at the beginning of December. The rhodium price doubled within the last 12 months to more than $3,000, and palladium gained nearly 40 percent to over $270 in just eight weeks.

This development is unprecedented over the last two decades. The fact that it has not caused sheer panic amongst industrial end-users is the result of the timely introduction of corporate hedging policies during 2003 and 2004. During those years, many major companies secured prices as far out as 2006; hence they are still relatively comfortable – for the time being. But with the hedges now gradually reaching maturity, interest in future developments in the platinum price is certainly growing amongst industrial end-users.

To address their need for first-hand information, Heraeus, the German-based precious metals refiner and fabricator, invited industrial clients to its first PGM Forum, which took place in Hanau, Germany on Thanksgiving Day, 24 November.

About 80 participants from nearly 50 companies accepted the invitation to discuss the latest developments in the pgm markets. The six presentations held covered a wide variety of topics, ranging from production and new uses of pgms to the development of the global economy and the potential impact on prices. Summaries of the main points of the presentations follow.

Peter von Zahn: Developments in the South African Mining Industry

Opening remarks from Dr Roland Gerner, Managing Director of W.C. Heraeus, were followed by a presentation from Peter von Zahn, Branch Manager of Anglo Platinum’s subsidiary RPM in Zug, who outlined the latest developments in the South African mining industry.

South Africa continues to be a major supplier of pgms, currently producing about 77 percent of the annual global platinum output. The country holds about 63 percent of reported worldwide platinum reserves and resources; together with neighbouring Zimbabwe that number increases even more to 80 percent. Of the South African reserves and resources, 73% are owned by Anglo Platinum, 13% by Impala, 9% by Lonmin, and 2% by Aquarius and 1 % each by Southern Platinum and Northam.

After announcing expansion plans in May 2000, the South African industry faced a number of challenges, which included the dollar price of pgms – particularly the initially low palladium and rhodium prices – the highly volatile nature of the rand exchange rate and a producer price inflation of 33.7 percent in just four years. Operating margins declined between 2000 and 2004, from 60.3 to 27.8 percent, leading to severe restrictions on cash flows.

These constraints necessitated the revision of the previously published expansion schedule. For Anglo Platinum alone that meant a reduction in the planned output for 2006 from the initial target of 3.5 Moz to 2.7 – 2.8 Moz, which was announced in February 2005. The guideline for Anglo Platinum remains the expansion of production in line with increasing global demand while maintaining the flexibility to be able to react to new trends on the consumption side.

When describing the political challenges for the mining industry, von Zahn emphasised that Anglo Platinum is firmly committed to a sustainable BEE. There are ongoing discussions about the Precious Metals Bill, which is intended to provide greater downstream beneficiation opportunities and assist the government’s implementation of its broad-based socioeconomic empowerment charter. However, a number of amendments proposed by the mining industry have been accepted and the Bill is now likely to be enacted early in 2006.