Issue 57

Will China Overtake India to Become the World’s Largest Manufacturer of Gold?

Since 1995, when India took over from Italy as the world’s largest manufacturer of gold (here defined as the fabrication of jewellery, industrial products and investment bars and coins – standard large bars are excluded from this analysis), the country has accounted over the period for around 23% of such global fabrication demand.

In recent years, though, a combination of falling off-take in India and rising Chinese demand has seen the gap between the incumbent and the challenger narrow significantly. Indeed, we argue in this article that, in 2009, it is probable the gold medal spot will be taken by the East Asian giant, although depending on future trends in the gold price, South Asia’s loss may only be temporary.

The table below shows GFMS’s latest estimates for gold demand in China and India. It reveals that in 2009 – basis data for the first three quarters plus forecasts for the fourth quarter – total demand in China is expected to exceed by a small margin that in India. Although the fourth quarter outcome will be critical to the final result, we doubt there will be a change in the leadership once these numbers have been gathered. This is because high prices in the last two months and in early December have tended to hit demand in India rather more than they have in China.

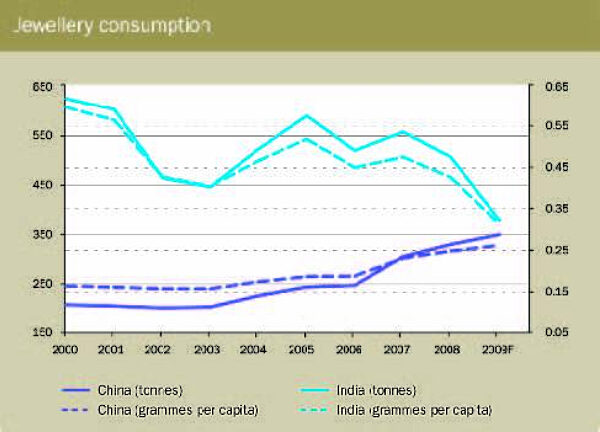

Greater Indian price sensitivity, in fact, is one of the main reasons behind the convergence in the country’s demand and that of China. The Indian market has been under pressure for several years from volatile and rising local gold prices, particularly its key 22-carat jewellery component. Meanwhile, Chinese demand, both in terms of jewellery and investment, has climbed higher and higher, not just in spite of local price strength but, arguably, also to some extent because of it. This is particularly true when it comes to the growing thirst of local investors for bullion bars, which has seen China comfortably overtake India in this category of demand.

Besides the influence of price, other factors have helped to narrow the gap between off-take in India and in China. An important one has been the faster rise in consumer spending in the latter than in the former. The more rapid growth in Chinese consumer spending has been particularly marked this year, with for instance around a 9% year-on-year rise recorded in China (for urban households only) in the first half, compared to an increase of less than 3% in India, where economic growth has been more severely affected by the global economic downturn. In addition, one should bear in mind the influence of China’s better overall economic performance in terms of GDP growth and the level of increase in its GDP per capita over many years. Moreover, China’s higher savings rate combined with a less open economy (meaning fewer investment alternatives to gold) have also helped to stimulate a stronger trend in investment demand in the country than in India, particularly in the last few years.

Chinese demand, both in terms of jewellery and investment, has climbed higher and higher, not just in spite of local price strength, but arguably, also to some extent because of it.

Jewellery demand in China has also grown faster than in India in recent years because the retail market in the former is far less developed than in the latter. What this has meant in China’s case is a continued massive expansion in the number of retail outlets, with these shops having to be stocked with product, and the greater availability of gold jewellery in a wider part of the country helping to stimulate additional consumption. In contrast, the retail structure in India is by now already fairly mature, at least in terms of the number of points of sale.

Finally, we would argue that social change has been more helpful to demand in China than in India. In the former, a growing moneyed middle class has been eager to establish its status and safeguard its wealth in the form of gold, both in terms of jewellery and, lately, in bullion too. Meanwhile, in India, the rising middle class has, at the margin, de-emphasised the traditional affinity for gold and instead embraced other forms of consumption. The decline in India’s per capita jewellery demand partly reflects this, although the shift away from jewellery towards bullion products has admittedly been of greater importance.

Turning to the future, even though there are secular trends at work that we believe will tend to dampen Indian off-take in the future, especially for jewellery, we would be the first to recognise that there is huge pent-up demand at present in the country, which is mainly being held back by very high local prices. Thus, in spite of the stronger underlying growth in Chinese demand for both jewellery and investment, it could be that if prices moderate sufficiently, off-take in the South Asian giant will rebound tremendously in 2010, or if not then, in the not too distant future, allowing India to seize back the number one spot. In the next year or so, gold prices will therefore be decisive in terms of the answer to the question posed in the title of this article.

For instance, were dollar prices to drop back in 2010 to an annual average of below $1,000 per ounce (and assuming more or less stable yuan and rupee exchange rates to the dollar), we would be fairly confident of India regaining its mantle. On the other hand, a ‘high price scenario’ with an annual average exceeding $1,200 would likely see China’s lead over India increase, due to the latter’s greater short-term price sensitivity.

We would argue that social change has been more helpful to demand in China than in India.

Philip Klapwijk has over 20 years’ experience analysing the gold, silver and PGMs markets, most of this time working for GFMS, which is the world’s leading specialist research consultancy on the precious metals markets. (GFMS, for example, is the prime source of statistics on gold and silver markets worldwide.) GFMS became independent of former owner Gold Fields of South Africa via a management buyout in August 1998 and Philip was the company’s first Managing Director. Since January 2004, he has been the Executive Chairman of GFMS. Philip is co-responsible for the strategic direction of GFMS and heads up its market research on the official sector, investment and fabrication demand in the Americas, Europe and China. Philip has also helped to oversee GFMS’s expansion in recent years into other areas, including base metals and steel research and, most recently, mining consulting and costs. (For more information see: www.gfms.co.uk.) Philip is a frequent speaker at conferences on precious metals and commodities, and the print and electronic media regularly quote his views on the gold, silver and PGMs markets.