Issue 68

Reinterpreting Gold’s Price Behaviour

Gold is not just money, it is ‘good’ money. In this article Daniel Brebner argues why Gresham’s Law is so relevant in understanding gold and how it behaves.

Gold is widely misunderstood. Many investors don’t understand how it is valued and why it behaves the way it does. Some are uncomfortable that gold is not ‘consumed’ like other commodities – it is not eaten, or burned or forged, as food, energy or industrial metals would be.

Gold has no use, according to many. But then gold is not really a commodity at all. While it is included in the commodities basket it is in fact a medium of exchange and one that is officially recognised (if not publicly used as such). I would argue that gold is an officially recognised form of money for one primary reason: it is widely held by most of the world’s larger central banks as a component of reserves.

I would go further, however, and argue that gold in fact could be characterised as ‘good’ money as opposed to ‘bad’ money which would be represented by many of today’s fiat currencies. In describing gold as such I refer to Gresham’s Law: when a government overvalues one type of money and undervalues another, the undervalued money (good) will leave the country or disappear from circulation into hoards, while the overvalued money (bad) will flood into circulation.

Support for this assertion comes from my interpretation of US government action at the end of dollar convertibility in 1971 (the end of the Bretton Woods system). The US ended convertibility because it did not want to send its gold to France or Britain who were demanding gold (or about to) rather than dollars; this in response to the decline in perceived value of the dollar due to profligate government spending during the 1960s. The US government valued its ‘good’ gold money more than its ‘bad’ paper money and therefore set about hoarding it – officially. Thereafter the USD, the bad money, became the world’s reserve currency (with immense benefits for US government funding, in our view).

This ‘good’ money assertion holds from this point, but for a short window during the late 1990s when several western governments (Britain, Canada, Switzerland, etc) decided to convert their gold to other (presumably more valuable?) fiat currencies – most likely the US dollar. I would suggest that the US government did not object.

Characteristics of ‘good’ money

The ideal medium of exchange must balance the paradox of representing value while having little intrinsic value itself. There are very few media which can do this. Fiat currencies physically have no use other than that which is prescribed to them by government and accepted by the public. That fiat currencies cost little to produce is of secondary concern and, I believe, quite irrelevant to the primary purpose. Gold is neither a production good nor a consumption good. Jewellery, I view as a form of storage or hoarding (the people of Portugal have all but exhausted their personal gold stores, hoarded in the form of jewellery, having converted it to survive the crisis). If gold did have a meaningful commercial use, I believe that it would make the metal less attractive as a medium of exchange, as the value of the metal in whatever market it was used in could periodically interfere with its medium-of- exchange role.

That gold is fairly costly/difficult to obtain is of secondary relevance to the value that it is used to represent. The fact that this characteristic has throughout history continuously frustrated governments reliant on a gold-standard and therefore unable to expand their spending at will is, again, secondary. Nevertheless I do believe that scarcity could be an important factor in ensuring the longevity of a currency. Scarcity may create some stability in the value that it represents and in turn influence the confidence with which the public regard it.

Other characteristics are important in fulfilling the requirements for ‘good’ money: indestructibility, divisibility, transportability and universal acceptability.

The conclusion from my overview of gold functionality is that the key difference between good and bad money is scarcity (imposed supply discipline could be another way of describing this). Fiat currencies can be scarce but this scarcity may change on a whim which may both impact its tenure as currency and/or relegate it to being characterised as bad money.

Gold is truly scarce, having a concentration of around 3 parts per billion in the Earth’s crust (see Figure 2). If all the gold ever mined were to be put in one spot it would consist of a cube roughly 20 metres per side. Furthermore and equally important, the rate of gold supply growth is normally quite slow and reasonably predictable.

Gold’s price behaviour

To describe it in the simplest of terms, gold’s value depends in large part on the degree of ‘badness’ of bad money. Following on from the previous discussion this factor is significantly reliant on relative scarcity.

If bad money becomes less bad (supply growth constrained and interest rates at appropriate levels), then one would expect that the desire/ incentive to hold good money becomes less obvious. Hoarding of good money would, according to theory, fall. Gold’s utility in this case would decline and prices would fall relative to the US dollar; the degree of this fall would likely be determined by the required supply contraction and therefore gold production costs (this secondary pricing factor becoming more important in determining value as the primary currency element diminishes in my view).

If, however, as seems to be the case currently, bad money becomes increasingly bad, then one would expect that the desire/incentive to hold good money should increase coincident with the perceived deterioration in functionality of the bad money as a currency. In short this is why the gold price has been appreciating over the past 10 years – coincident with the growing overvaluation or increased ‘badness’ of the US dollar.

Throughout history there has been one consistent factor which has contributed to the overvaluation of fiat currencies versus gold: excessive borrowing (often associated with war). In the past 100 years alone the US has experienced this twice: in 1934 and 1971.In 1934 the dollar was devalued by 42% versus gold and in 1971 the dollar was initially devalued by 8% and then by considerably more as the market pushed gold prices higher when inflation took hold into the late 1970s (a function of the easy monetary policy of the 1960s, war and a supply shock in oil).

History now appears to be repeating itself with excessive borrowing resulting in a new phase of devaluation for the dollar although the current situation may be unprecedented in modern history for the breadth and scale of the value adjustment that may be necessary.

Monetary factors

I would argue that the gold price is highly price sensitive to two monetary factors: 1) excessive fiat money supply growth (ie, a rate above that justified by population and unlevered productivity growth combined); and 2) money velocity. Velocity is an important factor given the higher the money velocity (greater transactions) the greater the accuracy in the relative pricing of economic goods, particularly during environments of changing money supply. Nevertheless I attach primary importance to supply.

Some economists would argue that it is not sufficient to look only at money supply, that demand for money is also important. I would disagree with this assessment; money is not a production/consumption good as I have previously discussed. What is the marginal demand for money? The question itself is a non-sequitur. There is constant demand for money whatever the economic condition. The important question is how this money is used once it is acquired.

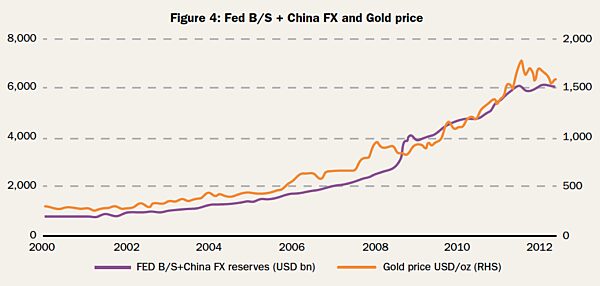

The conventional metric to view money supply is to look at M2, for both the US and China. In my view it is important to use both regions given the RMB peg, creating a kind of USD axis which dominates the global economy. Figure 3 combines the Fed balance sheet and China F/X reserves. This is a potentially superior representation of incremental money supply. Note that much of this expansion is backed by credit – credit fuelled spending by the US consumer for Chinese products resulting in increased China reserves combined with the Fed bailouts.

There may be some double counting in the combination of this data but I don’t believe that it is significant.

Figure 4 below then shows the relationship between the growth in USD supply and appreciation in the gold price. By association of course I imply causation which should always be treated with caution (as Hume would advise). I previously argued however that by using historic precedent excess supply can be associated with overvaluation; I make this assertion here.

Taking the ratio between the two data series I derive Figure 5. The ratio between gold and money supply remained fairly stable until late 2008, coincident with the collapse of Lehman and a peak in the intensity of the financial crisis at that time. Interestingly the expansion of the Fed balance sheet at that time actually resulted in an initial de-rating of gold against the supply of dollars. Yet this is opposite to what I have argued; instead we should have expected to see gold’s price move higher coincident with the increase in supply. What happened?

Figure 6 takes this analysis a step further by including US CPI (I admit that is a poor gauge of inflation, but it serves its purpose sufficiently here). In late 2009 deflation emerged in the Western economies as consumption contracted and money velocity sank. On this basis I believe that while the supply of money grew considerably, valuations in US dollar terms were impacted by the constraints on the flow of money through the economic system at the time. Much, if not all, of the new money created by the Fed went to banks which then purchased US short-term bonds. I would argue that this hoarding occurrence temporarily inversed the good/bad money dynamic between gold and the dollar. There was not increased hoarding of gold at this time as the principal beneficiaries of the increase in money supply must operate within the confines of the fiat regime and do not have the flexibility that the public and the state do.

Implications for forecasting

How does one go about forecasting gold prices? Implied in the above argument is the necessity to forecast future central bank action with respect to monetary policy, and also how additional money would subsequently flow through to the rest of the economy. The latter aspect – effectively, how will the individuals receiving this new money spend it – has important implications for inflation. In the case of 2008, the new funds were used by financial institutions to bolster their liquidity requirements, resulting in inflation in a particular asset class benefiting from such purchases: US treasuries.

In a future quantitative easing (QE) scenario the question is not only who will receive this incremental money but also, how it will be spent, given this could lead to selective price inflation with repercussions for gold price performance.

While I believe that the US Fed could continue to expand its balance sheet further in the future, the extent of money expansion is difficult to determine. But even more challenging is predicting how (or even if) this money will move through the broader economy.

For example, if the Fed were to announce a QE of a magnitude of USD1 trillion then the gold price would likely move to USD1,900/oz ±100/oz, assuming perceptions of inflation remained the same. If, however, inflationary fears escalated, a price of USD2,500/oz could be justified. In this latter scenario, I expect that this excess money would need to be more broadly distributed. It is possible that this could occur if the commercial banks which are principal beneficiaries of the Fed’s balance sheet expansion in turn expanded their balance sheets to the benefit of consumers and/or corporations.

For gold to react to its maximum potential new ‘bad’ money needs to be created and subsequently disseminated efficiently into an economy where a sufficient frequency of transactions results in a wholesale repricing of production/consumption goods.

Daniel Brebner is Head of Metals Research at Deutsche Bank, his focus however also includes bulk materials such as iron ore and coal.

Prior to joining Deutsche Bank, Daniel spent 10 years as an analyst at UBS where he held various positions, the most recent as co-head of Commodities Research. He was a geologist with Buenaventura Ingenieros in Lima Peru before working in the banking industry. Daniel has an honours BSc in Geology (University of Toronto) and an MSc in Mineral Exploration (Queen’s University). He is also a CFA charterholder.