Issue 70

Fear, Delusion and the Gold Investor Index

In this article, Adrian Ash and Ben Traynor explain how they have devised an Index to measure Western household sentiment towards physical gold. People buy gold for many reasons. But in the Western imagination, buying gold spells ‘fear’ like little else.

“Fear, Mr. Bond, takes gold out of circulation and hoards it against the evil day,” a Bank of England officer briefs 007 in Ian Fleming’s Goldfinger of 1959. Two decades later, “We’re in World War Eight if you believe the market,” the press quoted one Comex trader as gold hit its 1980 high. With the next upturn in prices, “Popular delusion [still] says gold remains the best hedge against Armageddon,” smirked the New Yorker magazine in 2004. But Armageddon began three years later, and come the US downgrade, euro crisis and English riots of mid-2011, “Gold is a mirror,” wrote a Californian finance professor. “Its price gauges fear of uncertainty, fear of losses and fear of poverty.”

The figure of the private investor – the dreaded goldbug – looms large in this popular conception. Yes, this character is also greedy (even with his nuclear bomb and S.M.E.R.S.H. connections, Auric Goldfinger attacks the US gold reserves at Fort Knox to become “the richest man in the world, the richest man in history!”). But lacking panicked queues outside bank branches during the virtual run of 2008, the media found anxious queues outside coin shops to be a useful replacement. When The Economist magazine first addressed gold’s bull market in 2009, it pointed to the fictional Harry ‘Rabbit’ Angstrom, anxiously hoarding gold Krugerrands in John Updike’s Rabbit Is Rich. And in mid-2011, one British reporter declared to us that the decade- long rally in gold prices was in fact entirely due to Tea Party supporters, glued to Fox News and fearing the imminent collapse of society.

Given such cultural touchstones, retail gold investors would seem central to the zeitgeist of the West’s continuing financial crisis. Anecdote, however, has had to suffice to date.

Because while private individuals are perhaps overrepresented in the popular view of gold investing (not to say misrepresented), they are little examined in the data.

“Given such cultural touchstones, retail gold investors would seem central to the zeitgeist of the West’s continuing financial crisis.”

Gold analysts can monitor a number of indicators to give them a feel for prevailing sentiment in the market. The weekly Commitment of Traders report from the Commodity Futures Trading Commission (CFTC), for example, gives a snapshot of gold futures’ positioning among money managers, as well as the ‘non-reportable’ positions of private speculators. The CFTC data only refer to leveraged trading, however, and the net long position of the ‘doctors and dentists’ (who risk getting filled and drilled) clearly reflects the availability of brokers’ credit more than sentiment towards physical gold bullion. Flows into and out of exchange-traded gold trust funds (ETFs) also give clues as to how bullish or bearish the market as a whole may be. But whilst not the proxy, perhaps, for the wholesale over-the-counter positioning that some analysts have claimed, a feature of ETF tonnages is that they give little weight to grassroots investors, whose size and activity is swamped by much bigger players.

As a result, financial journalists will often cite sales of American Eagle bullion coins as a guide to retail investment demand. This brings other drawbacks, however, as US Mint sales data are very lumpy, measuring sales to retail distributors rather than end consumers, and also displaying a high degree of seasonality when the new date is issued each January. Moreover, such sales figures can only measure retail activity on the buy side; they do not capture any reselling of coins by the public. A similar problem affects the World Gold Council’s authoritative Gold Demand Trends. This quarterly report, based on industry data gathered by Thomson Reuters GFMS, necessarily suffers a time delay. Western household investment is elusive again, both at the country level (offshore holdings can’t be clearly identified) and because much of the reported flow is mediated through retail distributors. Nor can retailers measure the true depth of coin and small-bar reselling on the secondary market. Tracking sales on eBay may be helpful, but volumes remain small and the pattern unclear. Yet gauging two-way activity is surely vital if we are to approach a clearer picture of household behaviour – and thus sentiment – towards physical gold investment.

WHILE WE HAVE SOME FUND CHARITY CLIENTS, WE ARE A CONSUMER-FACING BUSINESS ONLINE, SO THE INDEX IS ENTIRELY SEPARATE FROM INSTITUTIONAL OR CENTRAL BANK FLOWS

To augment the existing data sources, BullionVault launched its Gold Investor Index last October. First, we wished to provide, via a monthly data point, a window onto Western household sentiment towards gold, specifically across the US, UK and Eurozone, the currency areas where the vast majority of BullionVault users – some 89% – reside. Although we have some fund and charity clients, we are a consumer-facing business online, so the index is entirely separate from institutional or central bank flows. Entering and managing their own trades as they choose, our users are also self- directed, heightening our data’s sensitivity to customer sentiment. Indeed, the creation of our index was prompted by our colleagues and contacts in the professional wholesale market asking what action we were seeing on our peer- to-peer retail trading exchange online. A further motivator was the fact that the proverbial ‘hard-working saver’ – as well as non-specialist journalists and other observers using consumer behaviour to illustrate their opinions – tends to have little interest in gold absent moments of extreme economic tension. So the Gold Investor Index, by seeking to reflect retail investor attitudes towards physical bullion, might also be viewed as an indicator of wider economic and financial sentiment.

What does the Gold Investor Index show?

BullionVault users buy and sell gold held in Good Delivery bars, trading as little as 1 gram at a time in their choice of London, New York, Zurich and now Singapore storage. The index takes the number of net buyers, meaning those users who added to their gold holdings over the last month, and subtracts the number of net sellers. That figure – the balance of net buyers over net sellers – is then measured as a percentage of everyone who already owned gold at the start of the month. (First-time customers therefore push the index higher, as they only show in the numerator.) Finally, this number is added to 50.0, which is the index level signaling no change – a perfect balance of buyers and sellers, with sentiment amongst self-directed private investors neutral overall.

Note that, whilst closely aligned historically, the index does not track the weight of net client demand (see Figure 1). The Gold Investor Index gauges the number of people whose gold position rose or fell during the month, rather than the quantities of metal traded. Each individual actor is given an equal weighting – one user, one vote – so that the sentiment of larger customers does not distort the picture. Nor would a reading of 50.0 mean that users bought the same amount of gold on aggregate as they sold. BullionVault itself enables the quantity of client property to ‘breathe’ in line with net demand, carrying and restocking its own trading float directly from wholesale market counterparties, and then acting as a market maker on its exchange by quoting firm prices. But even though our account is excluded from the index’s calculation, it would only carry one vote if it weren’t.

“The Gold Index gauges the number of people whose gold position rose or fell during the month, rather than the quantities of metal traded.”

Using the methodology outlined above, BullionVault has calculated the Gold Investor Index going back to October 2009. Although we have trading data from much earlier, we disregard these because: a) BullionVault was not then the largest provider of vaulted gold ownership online; b) the pool of investors using BullionVault was much smaller, again making it less representative of broader retail sentiment; and c) index values were much less stable but consistently high, as even small net additions to the user base added rapidly to the number of net buyers. Today, in contrast, BullionVault has been used by more than 46,000 people worldwide, and their privately owned gold property totals 33 tonnes. That weight represents some 0.4% of global net retail demand since the business was launched a decade ago and gives a greater sample size than most other consumer surveys achieve. It is also critical to remember that the index is based on actual decisions to buy or sell. It shows revealed preference, rather than would- be intentions – something that isn’t provided by, say, tracking Google searches for ‘buy gold’ (Figure 2).

So what does the Gold Investor Index say about grassroots sentiment towards physical gold in the West?

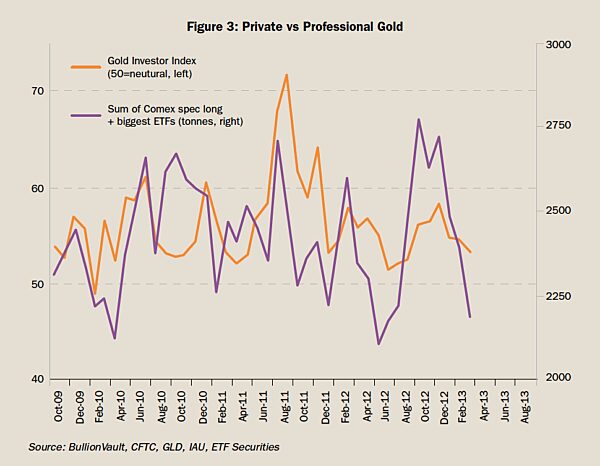

The index isn’t meant to supersede the existing data, but to complement these, focusing solely on private individuals and their actions. To date, commentators using our data have noted the preponderance of buyers over sellers every month since early 2010, but at levels far below the peak of late summer 2011. Referring to other data points in the market – which, again, the index is not meant to supersede but to complement – others have noted how private sentiment continued to rise even as exchange- traded funds and especially speculative longs in futures contracts were reduced. The reverse has also been true. Because as ETF gold holdings jumped to record highs in late 2012 (see Figure 3), and speculative positions in Comex futures neared 2011 levels, self-directed private households were not participating at anything like the same pace as the weight accruing in those vehicles might have suggested.

More recently, however, the distinctly bearish turn in speculative short positions on Comex, as well as the slashing of bank analysts’ price forecasts, has been reflected only moderately by private investor sentiment. With the speculative net long in Comex gold futures and options cut in half between November and March, the Gold Investor Index has yet to slip below 50. It turned lower in January, but sentiment has remained positive if subdued. The largest gold ETFs in contrast have shed more than 120 tonnes of gold between them, some 7% from their recent all-time records. Analysts may now look for the index to fall further perhaps if retail behaviour plays catch up with the retreat in so-called ‘safe haven’ demand amongst professional players. But it is no delusion that buying gold has continued to gain in popularity since the peak of the financial crisis to date.And whatever the fearful and greedy goldbug of popular imagination chooses to do from here, the Gold Investor Index gives voice to the real-world decisions of private individuals.

Adrian Ash, Head of Research, BullionVault.

Adrian Ash has been Head of Research at BullionVault since 2006. Formerly Editorial Chief at the UK’s largest publisher of private-investor advice, and also City Correspondent for the popular Daily Reckoning email, Adrian is now frequently quoted by leading news outlets worldwide.

Ben Traynor, Economist, BullionVault.

Ben Traynor is Economist at BullionVault and also Editor of its Gold News website. Ben read Economics at St Catharine’s College, Cambridge and is currently studying for an MSc in Financial Economics at Birkbeck College, London.