Issue 69

International Mine Production

The following is an edited version of a speech made at the LBMA/LPPM Conference in Hong Kong on 13 November 2012.

Introduction

I think there are a huge number of factors that ultimately have changed the way we are going to see mine production going forward, in particular gold mine production. In the years that this conference has been going, we have seen so many changes – the gold price going up, but also many changes with respect to the challenges that gold-mining companies face. As everybody knows, gold has been in a bull market for a number of years. In my view, that shows no signs of reversing.

Today, I would like to provide some context around how mine supply has responded to that higher gold price and to this environment, and what I see are the trends going forward.

Gold Mine Supply

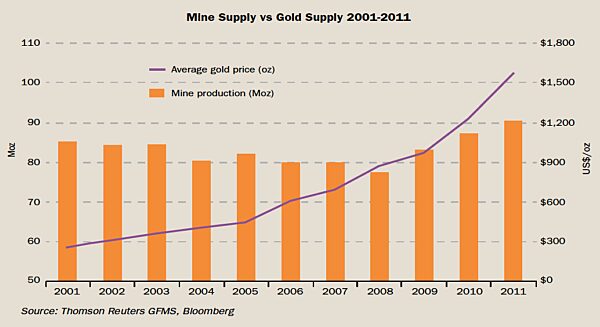

Over the past 11 years, gold prices have increased by almost 500%. However, gold mine supply has been largely unresponsive to that increase and was up only 6% over that period. I think many of us would have thought 10 years ago that if we were to see a gold price of over $1,700, there would be a lot more mine production in the world. That has not been the case. There are many factors that relate to that. I will talk about many of them today.

What are some of those factors? At a high level, I think we are seeing a combination of a lag effect of past low gold prices, cutbacks on exploration and capital spending in the past, plus a dearth of qualified technical people. The increasing maturity of the gold industry is another factor, as are the increasing cash costs that we have seen and the much higher capital costs. It is much more difficult now to find a mine, permit it and build it, than it ever was previously.

Industry Structure

There are very few mega-sized gold mines currently in production in the world. In terms of a cross-section of total gold mines by size, there are about 400 gold mines producing. Only 156 of these, or about 40%, produce over 100,000 ounces per year. We have 19 of those mines at Barrick. Twenty-one mines produce over 500,000 ounces per year. We have six of those. Only six mines in the world produce over 1 million ounces. We have two of those and are opening another two within the next couple of years.

As these mines continue to mature, there is limited potential to significantly increase the numbers of high-production mines in operation. We do not have a lot of big mines in the world that can ramp up production, and there are very few big mines being discovered. I will talk about that in a few minutes.

Annual Gold Production

In terms of annual gold production in the last seven years, one major trend is that there has been a significant changing of the guard amongst what were historically the biggest producing gold countries. In 2004, South Africa was the largest gold producer, but by last year had fallen to fifth- largest. Its ranking is likely to continue to decline given the increasing depth and higher cost of its producing mines. In 1980, just before Barrick was formed, 55% of all gold mine production in the world came from South Africa, although this was less than half of today’s overall production. Today, that is only 7% of 90 million ounces.

As you know, China has taken over the mantle as the leader in global mine production. It has done so with an abundance of small-scale and non-private sector operations. The largest gold mine in China produced just over half a million ounces in 2011.

Australia has maintained its production over the last five years, while the United States has dropped to third place. It is worth noting that whilst there is still discovery potential in Australia and the US, the mines in these countries are becoming increasingly mature. Thus, the additional production we are going to see is going to come from less-developed jurisdictions. With those new jurisdictions comes additional challenges.

Global Exploration Trends

In terms of global exploration trends, we have seen a significant decline in exploration discoveries, particularly of large deposits, in recent years. That is partly due to prior exploration spending cutbacks in the 1990s, with the lower gold price, and also because companies are now forced to look for new deposits in remote areas due to the maturity of the traditional mining jurisdictions. To a large degree, the low-hanging fruit has all been found.

Challenges

(a) Overview

Specifically, we have seen discovery rates decreasing. The supergiant, or 20-million-plus ounce deposits, are rare. Districts are becoming more mature. The average finding costs are increasing. The timeframes to develop mines are also increasing. 10 years ago, we could build a mine from discovery to production in three to five years. Now it probably takes seven to 10 years, at a minimum – and maybe even longer. There are technical challenges that a company faces, including increasingly deeper and covered targets.

There are also many more non-technical challenges, including socioeconomic and geopolitical ones, which are increasing in developed and emerging countries.

(b) Exploration

Despite global exploration spending being at an all-time high – $8 billion was spent on gold exploration in 2011 – the rolling three-year average of endowment (reserves, resources and past production) from gold and copper- gold discoveries in the past two decades has dropped off quite sharply. As a point of reference, there were 11 major discoveries in 1991 but only three in 2011. The trend of declining discovery rates has continued to persist even during this bull market in gold, despite the major ramp-up in exploration spending. I think this really reflects the increasing maturity of the industry.

It is also interesting to note that although there have been some gold discoveries, not one can be described as a super giant – that 20-million- plus ounce deposit. They are harder to find and that is directly impacting production growth because those super-giant discoveries are really the ones that can have a material impact on supply. There is also a lot less greenfield exploration being done. This is the so-called generative-type of exploration. That will also have an impact on future supply.

This decreased percentage of exploration budgets devoted to that early stage – or greenfield – exploration helps to explain the decline, over the last few decades, in the number of those big deposits. The trend in super-giant discoveries has been decreasing over the decades, from 14 in the 1980s, to 11 in the 1990s, to five in the 2000s. We will see what happens this decade.

The peak production in the 1980s was helped by the discovery of new technology, mainly heap leaching. We do not see any of those major technology breakthroughs today. The increasing maturity of the industry is evident. This will not bode well for future gold supply.

(c) Lag Times

Not only are discoveries decreasing, but the lag time between discovery – defined as the first resource that you can define – and production for mid-sized to large-scale mines is declining. Due to a number of factors, in the past, many discoveries of more than five million ounces were not put into production. Of the 105 five- million-plus ounce discoveries in the last 20 years, less than half of those are actually in production. In the past 10 years, we had 36 discoveries of more than five million ounces or higher. Only eight of these – 22% – are currently in production. This highlights how tough it is, even if you find gold, to advance it to production.

(d) Declining Grades

Grades of the ore produced in gold-mining and other mining industries have declined quite significantly. That is having an impact on production and cash costs. This is partly due to the maturity of the existing mines, and also because the gold price has gone up. The higher the gold price, the more ore that was previously uneconomical to mine now gets produced. You might previously have thrown it on the waste dump, or stockpiled it. Now, with the higher gold price, producers are lowering their cut-off grade so that they can produce the lower-grade ore that they previously could not at $300 or $400 per ounce.

There is a dramatic inverse relationship seen with gold prices increasing by about 500% in the past decade and average head grades moving from 2 grams per tonne to 1.5 grams per tonne. This does not sound like much, but it has a huge impact on overall cash costs. This means that companies are increasingly mining larger, low- grade deposits, which require larger equipment and facilities, and are costlier to build and maintain. Fewer and fewer companies are equipped to actually spend the money to build and operate these large, low-grade mines. Even the smaller mines are costing more to build.

(e) Industry Cash Costs

Industry cash costs have increased at nearly the same rate as the gold price. Since the end of 2005, the gold price has increased by 270%, but cash costs are up 187%. This is one of the reasons why the gold equities have tended to underperform. Cash costs have inflated, so those margins have not been as attractive as investors would have liked.

Even though this is on a percentage basis – so a higher gold price on a higher base has resulted in an expansion of those margins – cash costs have increased. Much of that is because of the gold price, resulting in the industry being able to mine lower-grade ores and using lower cut-off grades. Other factors that contributed to the cash cost increase include rising labour, consumable and energy costs, and royalties because of the gold price. Grade, cash costs and gold price are very closely related.

Over the past decade, cost inflation in the gold industry has averaged about 16% per annum, versus about 14.5% for other types of mining. These numbers are pretty close. A big part of those overall increases – about 10% in gold – is due to inflation, currency valuations, other general mine site costs, labour and consumables. The remaining 6% is related to declines in mining conditions, recoveries and average grade. We have seen a 16% per annum increase in cash costs. This is a bit higher in the gold business relative to other mining companies. With the possible exception of currencies, each cost factor can be expected to continue to increase mining costs in the future.

Barrick’s cash cost structure is similar to that of other organisations throughout the industry. Wages take up 40% of costs, and this is a figure that cannot be altered too much because of inflation with labour and union contracts. These rates will increase. There is a labour shortage in many areas in the world and wage increases cannot really be stopped. Energy takes up 15% and is also tough to control. It can, however, be hedged. We have done some things in that regard, but the industry is largely at the whim of energy prices. Maintenance costs account for 20%. That can be controlled a bit, but you have to do a lot of maintenance to ensure good availability for your trucks and other equipment. The cost of consumables for processing makes up the remaining 25%.

While you can do some things at the margin, the best way to control costs is to bring new, lower-cost mines into production and into your portfolio to replace some of your higher-cost declining assets. We are doing this. In the next few years, we are bringing in about 1.5 million ounces of new production at about $100 to $200 per ounce. That is where you will really see cost declines.

(f) Scarcity of Skilled Labour

The Minerals Council of Australia (MCA) undertook a study that shows a disconnect for supply and demand for workers and jobs required by the mining industry. In every category, the demand for labour exceeds the supply. This is why in Australia we have such high labour rates. In many of the areas we work in, particularly in Western Australia, the choice for the worker is to get on a plane and fly to one mine or another. It is fly in, fly out. He does not have to move or disrupt his family. Thus if one mine or company in the iron ore business says, “We’ll pay you more than the gold business”, all he has to do is walk perhaps another couple of hundred feet to another plane and get on that plane to work there. As a result, there is a lot of turnover. We have had 25% or 30% turnover in the past. That scarcity of skilled labour is likely to continue, although we are starting to see a little bit of relief on this front.

(g) Capital Costs

One often overlooked expenditure that is very important to our industry is the capital cost required to maintain production at operating mines. As the current mines mature, high gold prices allow for the production at lower depths and grades, but at increasing capital costs.

While we focus on cash costs as an industry, we must spend a significant amount on sustaining capital. According to a CIBC study, this represents another $200 to $300 per ounce to the industry’s overall cash costs, with expected go-forward increases of 7% to 10% per year. The increasing capital that you must add to just keep continuing to produce in the mine has impacted the amount of free cash flow that the industry can produce.

Project capital costs in the gold industry have also been increasing. Ernst & Young recently released a chart showing that of the companies that reported mine project overruns publicly between 2010 and 2011, the average overrun on those projects was about 71%. These projects are costing much more to build. We know this at first hand and it is not solely for one type of commodity. It is in all resource areas: iron ore, gold, copper, etc. This is a big challenge that we have to manage and it is also going to have an impact on supply.

When you add in exploration and G&A expenses, the all-in costs for the industry are approaching $1,500 per ounce. This was highlighted in a recent UBS report and compares with a figure of approximately $850 per ounce four years ago.

I think there is a perception that the gold industry is making huge cash margins. As you can see, that is not true. When you combine G&A, exploration, interest, capital and cash costs, we are producing at well over $1,000 per ounce. That dramatic impact is shown in the CIBC report. One example of how this has manifested itself is that even though gold prices increased by $1,000 in the space of the past seven or eight years, the free cash flow per ounce has only increased by $100 per ounce. Thus, we have been hearing from investors in recent months that they want more capital returned to them. We have heard them.

You have heard companies like us, and many others, talk about a focus on returns, free cash flow and being more disciplined. The days of growing production for the sake of nominal growth have been replaced with a renewed focus on capital allocation. This is going to result in less money ultimately being invested in lower-return projects at a time when ore grades are decreasing at mines. That is likely to result in a decrease in gold production in the industry going forward.

(h) Gold Equities

The difficulties that gold-mining companies have faced on the production and cost side have manifested themselves in making it more difficult for gold equity valuations. In 2004, the price-to-earnings multiples in the gold industry averaged about 80 times. They now average about 11 times and are thus below those of the S&P 500, which are 13. It shows that the lower multiple has been absorbed in the market, as it has seen the challenges that the gold-mining industry has faced. This has correspondingly made it more difficult for many companies, including junior companies, to issue equity, make acquisitions and invest in additional projects or exploration.

The underperformance of the gold equities versus the gold price is well known by many. Investors have opted for a simpler story rather than accept operational and other risks associated with a mining company. If they want to invest in the gold market, many investors buy the ETF, even though traditionally the gold equities have had more leverage. In my view, that should change as high stable prices and the focus on higher returns from the gold equities improves. I believe that we will revert back to gold equity outperformance over the gold price.

(i) Shrinking Valuation

The multiple contractions that we have seen, plus the increases in costs, have hit the valuations of junior gold-mining companies especially hard. A recent PricewaterhouseCoopers (PwC) report found that the market capitalisation of the top 100 junior miners on the Toronto Stock Exchange decreased by over 40% from the end of June 2012. This led to a 60% decrease in the number of those equities, with a market cap of over $100 million. That is also going to make it harder for companies to raise money and to explore and find more gold.

Top Business Risks

(j) Resource Nationalisation

According to Ernst & Young, the top business risk faced by companies involved in metals mining is resource nationalisation. This is key to a decision that a company like Barrick faces, whether we decide to invest capital in a particular country. Less industrialised countries, and often some developed nations, see rising commodity prices as a cure for their current economic problems. That shorter- term focus can blunt the long-term impact of companies like Barrick, who invest in these countries, and our willingness to invest in many of these countries. Often billions of dollars are involved. It will deter investment in those countries if the resource nationalisation threat is there, through tax or other means. Nationalisation is not solely an expropriation of assets. It also occurs through the imposition of punitive measures such as increases in royalty rates, taxes or the renegotiation of tax- stabilisation agreements.

(k) Skills Shortage

Another major issue that we face is a skills shortage. This is a current problem for all mining companies, which I have talked a bit about already. PwC reports that the four largest diversified mining companies by market capitalisation each had labour cost increases of over 8% last year. As I have mentioned, labour costs represent almost 40% of the cost structure and have a dramatic impact on cash costs. The break-even costs of producing gold are going up. In my view, that is providing a base on the gold price.

The demand for skilled labour has risen significantly. The knowledge and experience needed to build and operate mines is in short supply. There is an older generation of qualified geologists and mining engineers who are going to retire soon. There is a dearth of younger, qualified people in those areas. There is so much competition in the commodity space that we all have to really compete for that labour.

(l) Infrastructure Access

Infrastructure access is also an increasing problem. Discoveries are often in very, very remote areas. We are building a mine in very remote areas of Chile and Argentina at 4,500 metres. Conditions are very harsh and it is a six-and-a-half-hour drive to get there. We now have to go further afield to find these mines. We often have to put the infrastructure in place because there is no power, no water or no community. Thus, we have to spend significant amounts of money to do this.

(m) Capital Costs

This needed infrastructure increases the overall capital costs. Cost inflation is part of this. Capital project execution is important. As an industry, we are experiencing tougher and tougher times when building these mines. Mines often cost billions of dollars. Five or seven years ago, we could build a number of mines for $300 million or $600 million. We have just built one that cost almost $4 billion. We are building another one that will cost between $8 billion and $8.5 billion. This represents a dramatic increase in capital costs.

(n) Maintaining a Social Licence to Operate

Maintaining a social licence to operate has never been more important. There are more stringent environmental standards and a stronger focus on the social licence to mine. There is increased scrutiny on the industry. We must show that we are all committed to sustainable development or we will not be able to build or operate the mines. With that comes a growing number of responsibilities, including those that are regulated and some that are undertaken voluntarily. Other responsibilities include the Equator principles, the IFC’s Performance Standards and the OECD’s guidelines for multinational enterprises.

There is also a rise in socially responsible investors. We must make sure that we look closely at dealing with the impact of those social investors. We are not able to solely focus on cash costs and building mines on time. We must look at the environmental and social considerations more than ever, as are so many more investors. It not only is the right thing to do, but it is good business as well. NGOs continue to exert a tremendous amount of pressure on us. That is becoming much more complicated and we now must spend many, many more millions of dollars dealing with that

(o) Environmental Impacts of Mining

In terms of the environmental impacts of mining, we must reassure stakeholders, locally and around the world, that we are managing the environment well, including the impact on land, air and water. There is a relatively low amount of trust in the mining industry from the private sector. We are starting from behind the eight ball. We have to work with communities. We have to be part of the solution as we compete with those communities for scarce resources such as water and land.

The reliability of energy sources and the volatile policy and price environment is a challenge. We have to be seen as sharing the benefits in the countries and communities in which we operate. As I mentioned, expectations run very high regarding the benefits that mines can deliver to a country and host community, particularly in developing countries. Thus, we are part of a number of industry associations, some of which we have initiated, such as the ICMM’s initiative to better integrate sustainable development, the World Gold Council’s ‘Conflict- Free Gold’ standard to combat the potential misuse of mined gold to fund armed conflict, the Voluntary Principles cross-sector focus on improving the safety, security and protection of human rights around operations, and EITI’s focus on improving transparency of payments to governments. We are involved in all of these initiatives. As a mining industry, 10 years ago, we probably would not have had such a huge involvement with both civil society and government. That would have been unusual in the past, but we are now doing it in so many more cases. These are unique partnerships that we have to foster around the globe. However, it increases the challenges of bringing in new production.

Conclusion

The industry’s shift in focus is dramatic. We have seen huge changes. Investors are making it clear that they are no longer rewarding production growth to the same extent as in the past. Some gold producers, including Barrick, have responded by re-scoping, deferring or shelving marginal projects altogether. All of the things that I have talked about are major trends that are going to impact mine supply and be constraints to future supply. This industry is like a supertanker. It takes a long time to stop or change directions. You cannot turn on a dime. Most projects that are built right now, or are in advanced construction, will not be affected. However, the outlook for growth in supply in a few years looks more and more under threat. Thus, the supply of gold is likely to be lower going forward. We are not going to see huge growth, even if the gold price goes up considerably. That should then be supportive for the gold price and ultimately result in a healthier industry.

Jamie Sokalsky, President and Chief Executive Officer, Barrick Gold Corporation

Jamie C. Sokalsky was appointed President and Chief Executive Officer of Barrick Gold Corporation on June 6, 2012. He is also a member of the company’s Board of Directors.

Mr. Sokalsky joined Barrick in 1993 as Vice President and Treasurer, rising to Senior Vice President and Chief Financial Officer in 1999, and Executive Vice President and Chief Financial Officer in 2004, leading Treasury, Tax, Controllership and Financial Reporting, Internal Audit, Investor Relations and Information Technology.

Previously, Mr. Sokalsky was an executive at George Weston Limited for 10 years. He holds an Honors Bachelor of Commerce degree from Lakehead University and received his Chartered Accountant designation in 1982.