Issue 87

The Golden Revolution, Revisited: How to Prepare for the Remonetisation of Gold

This article is a synopsis of the Revisited edition of John Butler’s 2012 book, The Golden Revolution, in which he looks at how gold is, in various ways, being de facto remonetised, in particular for use in settling international balance of payments transactions. When combined with cutting-edge financial technology (‘FinTech’) this could, in time, catalyse a more general return to the use of gold or gold-backed money, with profound implications not only for gold but for financial assets and investment strategy.

The recent sharp decline in the value of the dollar and commensurate surge in the price of gold have rekindled speculation as to whether the dollar will indefinitely retain its Bretton- Woods legacy reserve status. As numerous prominent international economists have observed through the decades, beginning with Jacques Rueff and Robert Triffin in the 1960s, the dollar-centric international monetary system is inherently unstable, characterised as it is by chronic and growing trade and investment imbalances. While it is now commonplace to speculate as to whether the dollar’s reserve status may be imperilled by shifts in global economic power, few are prepared to seriously contemplate that, as the dollar’s reserve status fades, this could imply the de facto, even spontaneous, remonetisation of gold. However, when the precepts of modern game theory are applied to contemporary economic and political developments, and these are placed in the context of what I call the ‘monetary cycle of history’, one can make a persuasive case that gold remonetisation is not only inevitable, but imminent. The implications are potentially vast, not only for the price of gold but for other precious metals and financial assets generally.

Although the economic mainstream tends to be relatively quiet on the topic of global monetary regime change, it cannot fail to notice that nearly 10 years on from the 2008 global financial crisis, and following unprecedented economic and monetary policy intervention, global interest rates are still near zero; quantitative easing has failed to achieve its stated objectives; global imbalances have risen to record levels; emerging market balance-of-payment crises come and go with regularity; leading indicators in most major economies indicate weak growth ahead; and financial markets, in particular the credit markets, are beginning to tell us that another major crisis may lurk in the near future. It is thus entirely reasonable if unfashionable to hold the view that the international monetary system remains unstable and is overdue a fundamental restructuring or reset of some kind. None other than International Monetary Fund (IMF) Managing Director Christine Lagarde has hinted at this in multiple speeches over the past three years.

So, let us ask: why the relative silence on this matter? There are several plausible and complementary explanations. First, much human reasoning, expert or otherwise, is affected by at least some degree of so-called ‘normalcy bias’, that is, a naïve if not necessarily incorrect belief that the future will resemble the recent past. The dollar has been the world’s pre-eminent monetary reserve for some 70 years, so the thinking goes. Why should that change now? Second, and potentially reinforcing the above, is what one might call the ‘Whig view of international monetary history’. This is a subset of the better-known, more general ‘Whig view of history’, perhaps best represented by Scottish Enlightenment philosopher David Hume, that history is the evolution of an ever more perfect world of constant, if not always understood or appreciated, progress. Hence, the dollar-centric monetary regime of today is superior to those that have come before, because it is that of today, not yesterday. No further explanation is required or desired.

We know such thinking is flawed. History shows us that it is flawed: recessions, financial crises, depressions, wars, revolutions, currency collapses, etc. feature with some regularity. But this facile sense of steady (or sporadic) progress is nevertheless surprisingly common across all knowledge disciplines, not only in economic and monetary matters. Indeed, even in the hard sciences, where presumably only hard facts and evidence should matter, there can be tremendous resistance to new ways of thinking. Thomas Kuhn cogently demonstrated this to be the case in his monumental study of the history of science, The Structure of Scientific Revolutions. According to Kuhn, even in hard science, it is not the facts that matter. Rather, it is the ‘paradigm’, as Kuhn chose to call it. Facts that clearly do not fit the existing paradigm are either conveniently ignored, or those proffering them are persecuted outright, such as with Galileo’s observations of Jupiter’s moons.

“One can make a persuasive case that gold remonetisation is not only inevitable, but imminent.”

Given the relative subjectivity of the social sciences, including economics, one should wholly expect that the power of the presiding paradigm to misconstrue, ridicule or simply ignore inconvenient facts and their associated theories would be all the more powerful in stifling real understanding, productive debate and progress. Kuhn also noted that one reason why paradigms were so hard to break down once established was that those in highest regard within the discipline – akin to the high priests of a hierarchical church – had so much to lose if challenged by unorthodox thinking. We laugh at the Papal persecution of Galileo today, but at the time, it was no laughing matter.

Given that activist monetary policy has become the norm for most central banks, should we not fully expect them to resist ideas that might expose their policies as unsustainable or outright counterproductive? Yes, there are some scholars who are willing to challenge the paradigm, a few of whom are rather prominent. Nobel Laureate Robert Mundell, the so-called ‘father of the euro’, speaks openly about the dollar’s gradually eroding reserve status (although he stops short of claiming it will lose reserve status entirely). Professor Kevin Dowd, arguably the most prominent critic of the Bank of England and architect of monetary reform plans through the decades, has also expressed this view

The monetary sources of economic inequality

There is also another aspect of the current international monetary regime worthy of mention – the well-documented surge in ‘inequality’, however defined, across most if not all developed economies. The US Federal Reserve, through QE, has inflated asset values not only in the US but by extension globally. Those who are relatively ‘asset-rich’ if perhaps ‘income-poor’ have benefited disproportionately. However, those who are relatively ‘income-rich’ but ‘asset-poor’, such as the working middle class, have not. Indeed, the ability of the typical middle-class family to purchase a home, afford college tuition and access quality healthcare has suffered as asset valuations have risen. In order to maintain their previous lifestyles, many middle-class households must now borrow against their existing assets or, in more extreme cases, liquidate them entirely in order to raise sufficient cash to cover large life expenses. As the liquidated assets move from poorer to richer hands, asset values continue to rise, and QE further exacerbates the trend towards inequality.

(This monetary explanation for rising inequality is hardly new. It originates in the monetary theories of Richard Cantillon, a prominent pre-Smithian 18th century economist. Indeed, Adam Smith relied on and explicitly cited Cantillon’s insights across a broad range of his work. Numerous other prominent economists have also done so, including William Jevons, Carl Menger and Nobel Laureate Friedrich von Hayek.)

The inequality debate also has an international dimension. As the dominant global reserve currency, the dollar is used to pay for US imports from abroad and is then subsequently held in ‘reserve’ by the exporting country. As reserves accumulate, they are initially held as bank deposits but are subsequently reinvested in some way, for example, in government bonds issued by the importing country or perhaps purchases of corporate securities. In this way, the currency reserves earn some interest and possibly realise some capital gains.

Beyond a certain point, however, accumulated reserves will be perceived as excessive, in which case, exporters can exchange a portion of their reserves with another country or entity at some foreign-exchange rate. For this reason, other factors being equal, as the supply of reserves accumulates, but holding demand remains constant, the reserve currency will depreciate in value.

“So-called anti-globalists disparaging of free trade and economic interaction are thus not necessarily barking mad – well, perhaps some are – but they are barking up the wrong tree.”

Britain comes off the gold standard in 1931, other countries were to follow suit during the 20th century. The US would abandon gold in 1971-73 during the cold war

As time goes on, trade imbalances and reserve balances grow in tandem, as does the natural downward pressure on the value of the reserve currency as described above. This leads to what Belgian economist Robert Triffin called a ‘dilemma’: for global trade to expand, the supply of reserves must increase. Yet this implies a weaker reserve currency over time – something that can lead to price inflation. Indeed, under the Bretton Woods system of fixed exchange rates, the supply of dollar reserves grew and grew, price inflation increased and, eventually, as one European central bank after another sought to exchange its ‘excess’ dollar balances for gold, this led to a run on the remaining US gold stock and the demise of that particular monetary regime.

Now let’s combine Triffin’s insight with that of Cantillon. As discussed in previous chapters, money enters the economy by being spent. But the first to spend it do so before it begins to lose purchasing power as it expands the existing money supply. The money then gradually permeates the entire economy, driving up the overall price level. Those last in line for the new money, primarily everyday savers and consumers, eventually find that by being last in line for the new money, their accumulated savings are being de facto ‘diluted’ and the purchasing power of their wages diminished. Increased inequality is the result.

“Germany, 1923, during the period of hyperinflation. Paper money is worth more by weight than old bones, but less than rags.”

Extrapolated to the global level, this non- neutrality of money implies that an issuer of a reserve currency is the primary beneficiary of monetary inflation. First in line for the new international money are the owners of capital in the reserve-issuing countries, who use the new money to accumulate more global assets. On the other side are workers the world over who receive the new money last, after it has placed general upward pressure on prices. Growing global wealth disparity is the inevitable result.

Over time, this will impact the relative competitiveness of other economies, where wage growth is likely to accelerate, eventually making US labour relatively more competitive. That may sound like good news, but all that is really happening here is that US wages end up converging on those elsewhere, something that should happen in any case over time between trading partners as their economies become more highly integrated. But to the extent that this wage convergence process is driven by artificial global monetary inflation, rather than natural, non-inflationary economic integration, the result is real wages converging downward rather than upward, implying a global wealth transfer from ‘owners’ of labour – workers – to owners of capital. So-called anti-globalists disparaging of free trade and economic interaction are thus not necessarily barking mad – well, perhaps some are – but they are barking up the wrong tree. The problem is the dollar-centric international monetary system, not globalisation per se.

The monetary future

That both domestic and international imbalances continue to grow is not lost on economic officials, who do make reference to them from time to time. Intriguingly, the IMF has begun to promote the idea that the dollar might indeed eventually lose its premier reserve currency status. But the IMF is proposing in no uncertain terms that the ‘solution’ for the erosion of the dollar’s reserve currency status is to replace it with the IMF’s very own ‘Special Drawing Right’ or SDR. And yes, the IMF puts itself forward as the institution to control the world’s money supply and, by implication, global interest rates.

This may all sound nice on paper but what about in practice? The idea, amid record global economic imbalances and associated historic, arguably unserviceable, debt burdens in Japan, the euro area and the US itself, that China, the other BRICS, oil producers and other creditor nations will agree to any international monetary restructuring that does not favour their economic interests is a non-starter. The requisite international co-operation required for the IMF to implement a sustainable ‘one size fits all’ international monetary policy is just not there, nor should we be at all optimistic that it will be prior to a meaningful global deleveraging and rebalancing.

The recent experience of the euro area should serve as an example in this regard, but as observed above, facts can be quite an inconvenience for those clinging to a flawed paradigm. In the SDR debate, we see cognitive dissonance in the fashionable belief that what demonstrably does not work at the regional level can work miraculously at the global one. The fact is, monetary central planning does not work. It didn’t work for Europe in the 1920s and 1930s amid devaluations and hyperinflations. It didn’t work in the 1960s, as the London Gold Pool struggled to hold the Bretton Woods conventions together. It didn’t work in the 2000s, when the so-called ‘Great Moderation’ in business cycles merely disguised colossal misallocations of capital, exposed as such in 2008. And now nearly 10 years on from that spectacular crisis, it is not working still. There is good reason to believe that the next crisis is going to be more severe than 2008/09. This time around, interest rates are already near zero, or outright negative. The accumulated imbalances, domestic and international, are even larger. QE has failed to restore self-sustaining economic growth.

The monetary Nash equilibrium

If the dollar is indeed losing pre-eminent international monetary reserve status and the requisite co-operation required for the IMF to replace it with the supranational SDR is lacking, then what is going to happen? Without a stable international money, countries will find they cannot trade as easily with one another. What currencies will be held as reserves against accumulated external trade imbalances? Chronic net importers such as the US have the incentive for the world to hold their currencies as reserves, whereas chronic net exporters have the opposite. As the imbalances accumulate, as they now have to a record level relative to global GDP, beyond a certain point, there is insufficient trust in the importing countries’ currencies as reliable stores of value. But then if distrustful exporters insist on invoicing for exports strictly in their own currencies, trade will grind to a halt. It is by definition the importing nations, not the exporting nations, which must provide the net balance of circulating media for international trade, as these media represent the international ‘IOU’ that must eventually be repaid through a reversal in the trade (or capital) balance or otherwise liquidated (e.g. via a default).

“If just one exporting country, even a relatively small one, begins to demand payment in gold, then its trading partners must supply the gold.”

We know global trade is hugely beneficial for consumers, who benefit from the associated, evolving global division of labour and capital. A contraction in global trade, ‘globalisation in reverse’ as it were, would thus be highly damaging to global economic growth, implying a general ‘stagflation’ of both weaker growth and higher real goods prices. No politician, socialist or otherwise, wants that – it would force them from office in short order. So absent demonstrably unworkable central planning, how can future international monetary arrangements nevertheless facilitate international commerce, with exporters and importers at loggerheads over which currencies to use?

Why, the same way they did so in the 1800s. Just remonetise gold. For gold is the only international monetary asset that can resolve the exporter/importer dilemma of a lack of trust on the one hand, yet a deep, essential need to trade on the other. Gold is not itself a national liability. It can be neither arbitrarily devalued nor defaulted on. It is real international money, not bureaucratic fiat scrip. But wait, one might protest, why would governments willingly give up the power to devalue and inflate their way out of debt? Because if their essential trading partners so demand it, they simply have no choice.

What if Russia, concerned about the future of the euro, were to demand its European customers pay for imports of oil and gas in gold instead of euros? What if China, concerned about the dollar, accelerated its accumulation of gold? What if the Gulf oil producers were to insist that China pay for imports of their oil in gold? The fact is, if just one exporting country, even a relatively small one, begins to demand payment in gold, then its trading partners must supply the gold. For each incremental move in this direction, gold’s share of international monetary reserves grows exponentially due to the network effect. Conversely, the dollar’s share exponentially declines. And as those familiar with game theory will note, while there is no doubt a ‘first mover disadvantage’ associated with demanding trade settlement in gold – a possible loss of market share – there is a far larger ‘last-mover cost’, that is, the last exporter to switch from dollars to gold will find that they have accumulated the residual dollar reserves from the rest of the world at a greatly reduced if not worthless value.

Gold is the natural international money for a multipolar world

As Nobel Laureate Mundell wrote a few years back: “We can look upon the period of the gold standard as being a period that was unique in history, when there was a balance among the powers and no single superpower dominated.” The IMF recognises that the US is no longer the sole global economic superpower that it once was, able to dictate terms in monetary matters. A new multipolar balance of power is forming. Gold, the only internationally recognised non-national money provides the game-theoretic international monetary solution to an economically multipolar, globalised, competitive world. It represents the Nash equilibrium. Whether or not this is ever formalised in a de jure ‘gold standard convention’ or not is beside the point. The classical 19th century gold standard was never de jure formalised as such. As renowned monetary historian Guilio Gallarotti observes, it arose spontaneously from below, catalysed by the rise to economic power of the United States and the German Zollverein in the late 19th century, thus transforming what had been, following the Napoleonic wars, a nearly unipolar British imperial world into a clearly multipolar one.

As the global demand function for gold will shift due to de facto remonetisation, by implication, the price of gold will rise. By how much depends largely on the degree of confidence in the dollar and other currencies that circulate alongside gold. As long as the global imbalances and associated debts remain large relative to incomes, confidence will be low, implying a far higher gold price than that observed today.

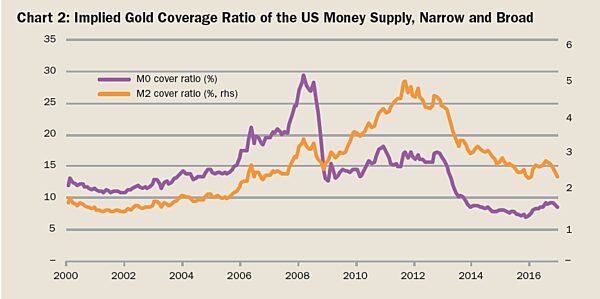

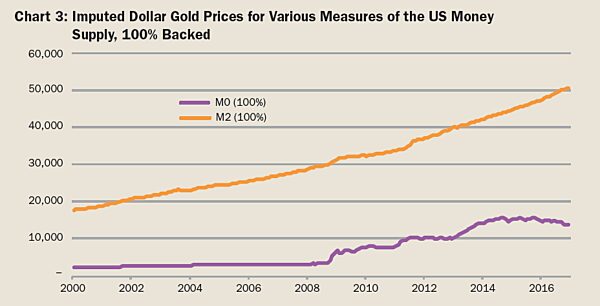

Using the historical gold-coverage ratios associated with the Bretton-Woods system and the prior history of gold-backed US currency, a five-figure oz dollar price for gold is entirely reasonable (see charts 1-3). By implication, as asset valuations adjust lower to a world in which money injections such as QE are no longer possible, not only will currencies decline in value versus gold. So will corporate securities and, in inflated markets, property, perhaps by amounts comparable to the relative decline of asset valuations versus gold in the late 1970s/ early 1980s, when gold remonetisation briefly went from being a fringe to a mainstream monetary policy topic.

Not only will gold rise in price. By implication, the international money (gold) market will determine spontaneously what interest rate clears the market for gold delivery today, or tomorrow, or next year. This information will then flow into international commerce generally, where it will provide a robust basis for the sensible allocation of international capital in all forms, financial and real, across both time and space. The escalating boom and bust cycles of modern times will become a thing of the past and the natural occasional recessions that do occur will allow for the Schumpeterian ‘creative destruction’ required to qualitatively reorder the capital stock so as to clear malinvestments and incorporate new technologies.

Gold and the information theory of capitalism

As George Gilder demonstrates in his masterful work on economics and information theory, Knowledge and Power: “Capitalism is not primarily an incentive system but an information system.” Prices are the information. And the price of time itself is the single most valuable piece of information. Time, as we intuitively know, is money; they are two sides of the same coin. Mess with time and money, and you mess with everything else. To borrow from Tolkien, the time value of money is: “The one price that rules them all.” Yet, as with central planning in general, the central planning of either money, or time, cannot possibly work. Hayek warned the economics profession of precisely this in the 1970s. It didn’t listen, ensconced – as it still remains – within its generally interventionist, neo-Keynesian paradigm. The result has been a series of financial crises, each one larger than the one which came before. The next, if the pattern is any guide, will be larger still – a crisis of the international monetary regime itself, one which will catalyse the remonetisation of gold.

The article is adapted from John Butler’s new, revisited edition of his 2012 book, The Golden Revolution (John Wiley and Sons, 2012). It is available on Amazon - amazon.com/ dp/1535608994/ and at other online and high street bookstores.

John Butler has over 20 years experience in international finance. He has served as a Managing Director for bulge-bracket investment banks on both sides of the Atlantic in research, strategy, asset allocation and product development roles, including at Deutsche Bank and Lehman Brothers. He has advised some of the world’s largest institutional and private investors in matters ranging from wealth preservation to enhancing returns through a wide variety of innovative strategies and he has been a #1 ranked investment strategist by Institutional Investor magazine.