Issue 97

The Rational Case For $7,000 Gold By 2030

It surprises many professional investors that gold has been the leading major asset class in the 21st century. It has beaten the US treasuries, US equities, developed market equities and emerging markets, even after accounting for dividends. $100 invested at the turn of the century has turned into $591.

Gold doesn’t pay a yield, unless you lend it, making this an extraordinary achievement. And because it doesn’t pay a yield, many believe that gold can’t be valued. I disagree and would attribute gold’s great leap forward to the fall in US real interest rates (104%), realised inflation (52%), starting discount (55%) and, finally, the recent move to a 24% premium. I’ll address these points in turn and then look at the decade ahead.

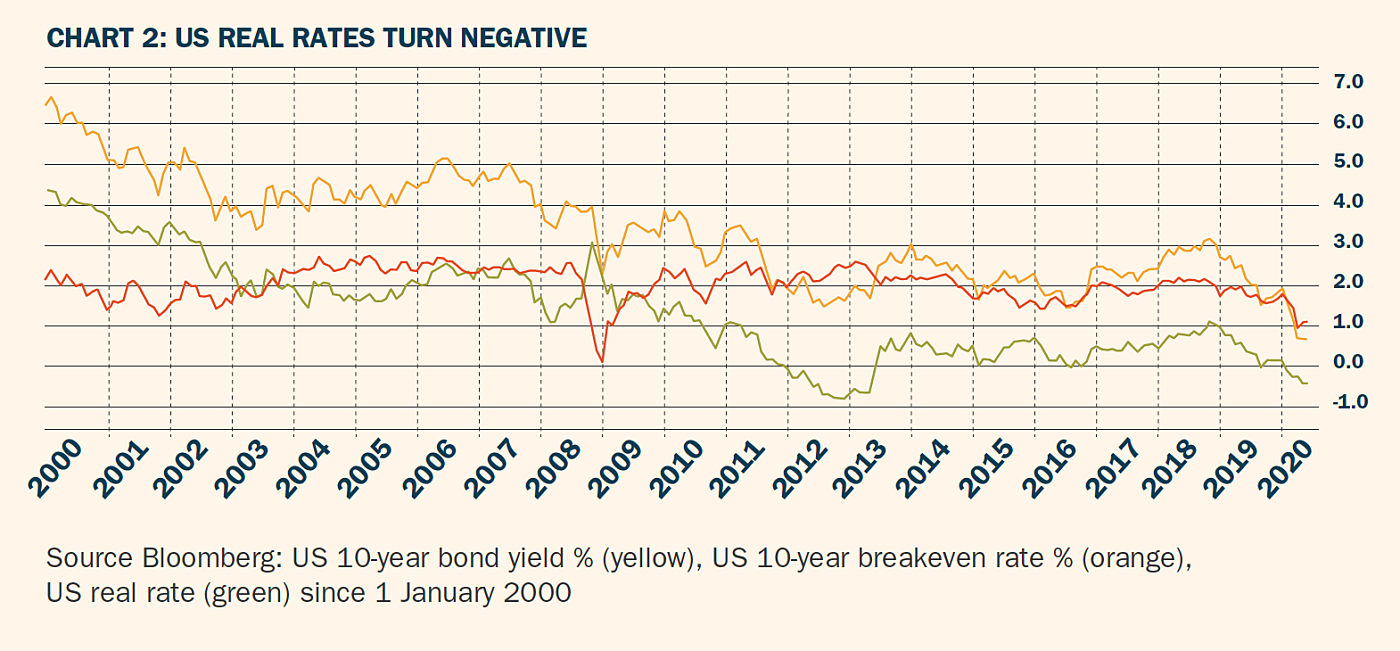

+4% US treasury yield less the expected rate of inflation was over 4% in 2000 and has recently turned negative

Falling Real Rates

The main driver has been falling real rates, that is, the US Treasury yield less the expected rate of inflation. This was over 4% in 2000 and has recently turned negative. It is wholly unsurprising that gold is deemed to be more attractive when cash on deposit receives a negative real return, compared to those glorious days when you could earn a 4% real rate without taking any risk. Little wonder gold was trading so cheaply in 2000

Modelling The Gold Price

In 2014, I first modelled gold as a bond with the following characteristics:

- It is zero-coupon because it pays no interest

- It has a long duration because it lasts forever

- It is inflation linked, as historic purchasing power has demonstrated

- It has zero credit risk, assuming it is held in physical form

- It was issued by God.

This describes a zero-coupon, risk-free, inflation-linked bond – something that resembles a 20-year TIPS. Last year, I wrote a more detailed piece, ‘How I Value Gold’, for the World Gold Council.

The link between gold and the fair value model is strong. Gold started the period below fair value and crossed above in 2008. It then got ahead of itself at the 2011 peak, only to fall back into line for the next few years. Recently a premium has begun to re-emerge.

I like the way the model declined in 2008, 2013 and recently during the COVID-19 crisis. Many believe gold to be a safe haven. Indeed, it is, but only when real rates are falling. If the system freezes up, and there is a fear of deflation, then cash is king. Yet, gold has typically been quick to recover once the threat of deflation passes – a sign of asset quality.

Another observation is that, at the time of gold’s 2011 high, the US consumer price index brushed 3.9%. While gold soared, asset prices retreated, and the euro crisis was set in motion. Gold has a unique ability to sniff out inflation, and as soon as the threat passed, gold retreated, while general asset prices rallied.